Build Your Custom Market Intelligence Report

Customize Your ReportSpain Medical Devices Market Key Highlights

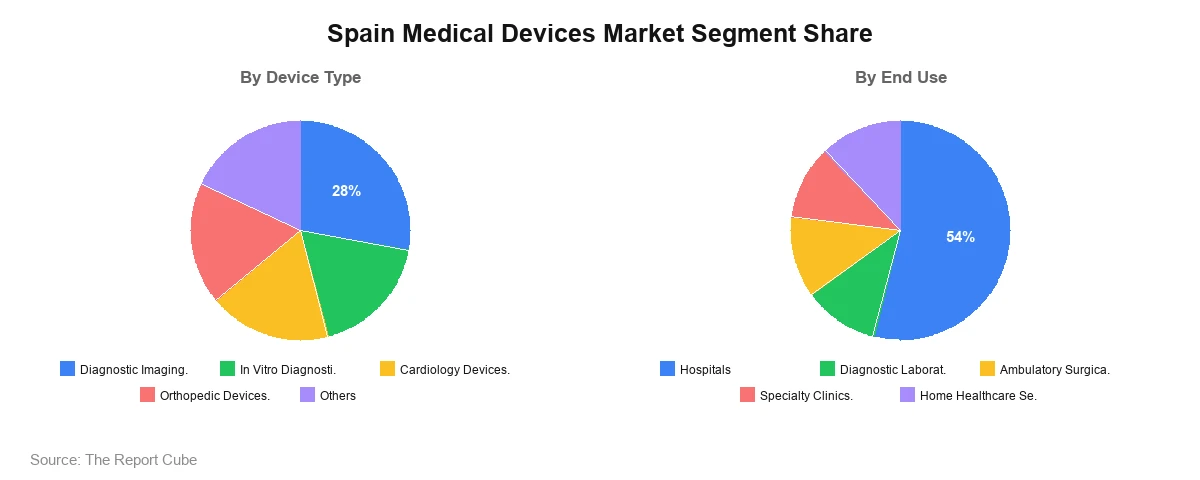

By Device Type:

Diagnostic Imaging Devices segment leads the market with nearly 28% share.

By End Use:

Hospitals segment dominates the market with around 54% of total revenue.

Regional Outlook:

Central region dominates the Spain Medical Devices market with approximately 32% share.

Spain Medical Devices Market Insights & Analysis

The Spain Medical Devices Market is anticipated to register a CAGR of around 6.2% during the forecast period 2026-2034. The market size is valued at USD 13.28 billion in 2026 and is projected to reach USD 21.48 billion by 2034. Spain continues to strengthen its position as one of Europe’s key healthcare markets, supported by rising public healthcare expenditure and modernization of hospital infrastructure. In 2025, Spain allocated over 7.5% of its GDP to healthcare, which has directly accelerated procurement of advanced diagnostic and therapeutic devices. Investments in digital radiology, minimally invasive surgical tools, and patient monitoring technologies are shaping a more efficient and data-driven healthcare ecosystem.

The market is also benefiting from strong participation of multinational companies and local distributors, creating a competitive environment that drives innovation and accessibility. Companies are increasingly focusing on integrating smart technologies such as connected devices and real-time monitoring solutions. Additionally, Spain’s aging population, where nearly 21% of citizens are aged 65 and above as of 2025, is creating sustained demand for cardiology, orthopedic, and home healthcare devices. This demographic trend, combined with government-backed digital health programs, is expected to support steady expansion of the medical devices sector throughout the forecast period.

Spain Medical Devices Market Dynamics

Key Driver: Rising Demand for Advanced Diagnostic and Minimally Invasive Technologies

The Spain medical devices market is experiencing strong growth due to increasing demand for advanced diagnostic imaging and minimally invasive procedures. Hospitals across Spain are upgrading legacy systems with modern CT scanners, MRI systems, and AI-enabled ultrasound devices to improve diagnostic accuracy. By 2025, more than 60% of tertiary hospitals in Spain had adopted advanced imaging technologies, improving patient outcomes and reducing diagnosis time significantly.

Additionally, minimally invasive surgeries are gaining traction as they reduce hospital stays and recovery time. The use of robotic-assisted surgery and advanced endoscopy devices has grown by nearly 18% annually in major urban hospitals. This shift is encouraging device manufacturers to innovate and supply compact, high-precision instruments that align with evolving surgical practices in Spain’s healthcare system.

Book your FREE 30-minute expert consultation today

Contact UsIndustry Trends: Integration of Digital Health and Smart Medical Devices

A key trend shaping the Spain medical devices market is the integration of digital health platforms with medical equipment. Hospitals are increasingly adopting connected devices that allow real-time monitoring and data sharing. Remote patient monitoring devices, for example, have seen adoption increase by over 22% between 2023 and 2025, particularly for chronic disease management.

Another emerging trend is the incorporation of AI into diagnostic workflows. Imaging devices now come equipped with automated detection systems that assist clinicians in identifying abnormalities faster. These advancements are not only improving efficiency but also reducing the workload on healthcare professionals, which remains a critical concern in Spain’s healthcare sector.

Major Challenge: Regulatory Complexity and Cost Pressures in Device Approval

The Spain medical devices market faces challenges due to stringent regulatory requirements under the EU MDR framework. Manufacturers must meet extensive clinical validation and documentation standards, which can extend product approval timelines by 12 to 18 months. This creates barriers for smaller companies attempting to enter the market.

Cost pressures also remain a concern, particularly for public hospitals operating under budget constraints. Advanced medical devices often come with high procurement and maintenance costs, limiting widespread adoption. These financial limitations can slow down the replacement of outdated equipment, particularly in smaller healthcare facilities across regional Spain.

Opportunity: Expansion of Home Healthcare and Remote Monitoring Solutions

The growing preference for home healthcare presents a strong opportunity for the Spain medical devices market. With an aging population and rising chronic disease prevalence, demand for home-based monitoring devices such as wearable sensors and portable diagnostic tools is increasing rapidly. By 2025, home healthcare services accounted for nearly 15% of total healthcare delivery in Spain.

Furthermore, advancements in telemedicine are enabling seamless integration of these devices with healthcare systems. Companies are developing user-friendly, connected devices that allow patients to monitor vital signs and share data with physicians remotely. This trend is expected to open new revenue streams and expand access to healthcare services, particularly in rural regions.

Spain Medical Devices Market Segment-wise Analysis

By Device Type:

- Diagnostic Imaging Devices

- In Vitro Diagnostics

- Cardiology Devices

- Orthopedic Devices

- General Surgery Devices

- Neurology Devices

- Gynecology and Urology Devices

- Endoscopy Devices

- Anesthesia and Respiratory Devices

- Patient Monitoring Devices

- Renal Care and Dialysis Devices

- Wound Management Devices

- Infusion and Drug Delivery Devices

- Consumables and Disposables

Diagnostic imaging devices dominate the Spain medical devices market, accounting for approximately 28% of total market share in 2025. This dominance is driven by continuous investments in imaging infrastructure and the increasing demand for early disease detection. Advanced imaging technologies such as MRI and CT scanners are widely adopted across public and private hospitals. Spain performs over 45 million diagnostic imaging procedures annually, highlighting the critical role of these devices.

Moreover, technological advancements such as AI-assisted imaging and portable ultrasound systems are enhancing diagnostic capabilities. Healthcare providers are prioritizing devices that offer faster imaging results with reduced radiation exposure. This trend is expected to sustain the segment’s leadership position throughout the forecast period.

By End Use:

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Specialty Clinics

- Home Healthcare Settings

Hospitals represent the largest end-use segment in the Spain medical devices market, contributing around 54% of total revenue. The dominance of hospitals is attributed to their comprehensive healthcare services and high patient inflow. Spain has over 800 hospitals, many of which are equipped with advanced medical technologies to support complex procedures.

Additionally, hospitals are the primary adopters of high-value medical devices such as imaging systems, surgical robots, and intensive care monitoring equipment. Continuous government funding and infrastructure upgrades further strengthen this segment. As healthcare demand continues to rise, hospitals are expected to maintain their leading position in the market.

Regional Projection of Spain Medical Devices Industry

- Northern

- Northeastern

- Central

- Levante

- Southern

- Others

The Central region leads the Spain medical devices market, holding approximately 32% of the total market share. This dominance is largely due to the presence of major healthcare facilities and higher healthcare expenditure in cities like Madrid. The region has a dense network of hospitals and diagnostic centers equipped with advanced medical technologies.

Furthermore, the Central region benefits from strong government support and access to skilled healthcare professionals. Investment in healthcare infrastructure and adoption of digital health solutions are higher compared to other regions. These factors contribute to the region’s leadership and are expected to sustain its growth during the forecast period.

Government Initiatives & Policies

- Spain Digital Health Strategy 2025: Government initiative promoting AI-enabled diagnostics, interoperable hospital systems, and digital patient monitoring adoption across public healthcare infrastructure.

- EU Medical Device Regulation (MDR) Implementation 2025: Strengthened compliance framework improving device safety, traceability, and clinical evaluation standards across Spain’s healthcare ecosystem.

Spain Medical Devices Industry Recent Developments

- 2025: Grifols announced a EUR 160 million investment to establish a new manufacturing facility in Barcelona, significantly increasing plasma fractionation capacity and strengthening its production capabilities in Europe.

Need insights for a specific region within this market?

Request Regional DataWhy Choose This Report?

- Provides a comprehensive overview of the overall market analysis, encompassing key trends, consumer behavior analysis, and risk assessment to support strategic decision-making.

- Provides accurate, up-to-date insights into market size, segmentation, and emerging opportunities, helping to minimize risk & capitalizing on growth.

- Gives deep understanding of target audience preferences, investment habits, and communication channels for enhanced product development & marketing effectiveness.

- Delivers competitive analysis & benchmarking, uncovering the strengths & weaknesses of market competitors to guide strategies.

- Consolidate comprehensive market intelligence, reducing reasoning & streamlining research efforts.

- Facilitates customized market segmentation & risk mitigation strategies, fine-tuned to the business objectives.

- Aids in identifying both market challenges & untapped opportunities within the industry to drive long-term business growth.

- Provides valuable information based on actual customer data & search trends.

Table of Contents

- Introduction

- Objective of the Study

- Product and Category Definition

- Market Segmentation

- Study Variables

- Research Methodology

- Secondary Data Points

- Breakdown of Secondary Sources

- Primary Data Points

- Breakdown of Primary Interviews

- Secondary Data Points

- Executive Summary

- Market Dynamics

- Drivers

- Challenges

- Opportunity Assessment

- Recent Trends and Developments

- Regulatory and Policy Landscape

- Spain Medical Devices Market Overview (2021-2034)

- Market Size, By Value (USD Billion)

- Market Share, By Device Type

- Diagnostic Imaging Devices

- X-ray Systems

- Computed Tomography (CT) Scanners

- Magnetic Resonance Imaging (MRI) Systems

- Ultrasound Systems

- Nuclear Imaging Systems

- In Vitro Diagnostics

- Clinical Chemistry Analyzers

- Immunoassay Analyzers

- Hematology Analyzers

- Molecular Diagnostics Systems

- Point-of-Care Testing Devices

- Cardiology Devices

- Interventional Cardiology Devices

- Electrophysiology Devices

- Cardiac Rhythm Management Devices

- Cardiac Monitoring Devices

- Orthopedic Devices

- Joint Reconstruction Implants

- Trauma Fixation Devices

- Spine Implants

- Sports Medicine Devices

- General Surgery Devices

- Open Surgery Instruments

- Minimally Invasive Surgery Instruments

- Wound Closure Devices

- Neurology Devices

- Neurostimulation Devices

- Neurovascular Devices

- Gynecology and Urology Devices

- Gynecological Surgery Devices

- Urology Surgery Devices

- Endoscopy Devices

- Rigid Endoscopes

- Flexible Endoscopes

- Endoscopy Visualization Systems

- Anesthesia and Respiratory Devices

- Anesthesia Delivery Systems

- Ventilators

- Respiratory Monitoring Devices

- Patient Monitoring Devices

- Multiparameter Monitors

- Vital Signs Monitors

- Remote Patient Monitoring Devices

- Renal Care and Dialysis Devices

- Hemodialysis Systems

- Peritoneal Dialysis Systems

- Dialyzers and Consumables

- Wound Management Devices

- Advanced Wound Dressings

- Negative Pressure Wound Therapy Devices

- Infusion and Drug Delivery Devices

- Infusion Pumps

- Syringe Pumps

- Implantable Drug Delivery Devices

- Consumables and Disposables

- Catheters

- Needles and Syringes

- Surgical Gloves and Drapes

- Diagnostic Imaging Devices

- Market Share, By End Use

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Specialty Clinics

- Home Healthcare Settings

- Market Share, By Region

- Northern

- Northeastern

- Central

- Levante

- Southern

- Others

- Market Share, By Company

- Revenue Shares and Analysis

- Competitive Landscape

- Northern Spain Medical Devices Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Device Type

- Market Share, By End Use

- Northeastern Spain Medical Devices Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Device Type

- Market Share, By End Use

- Central Spain Medical Devices Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Device Type

- Market Share, By End Use

- Levante Spain Medical Devices Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Device Type

- Market Share, By End Use

- Southern Spain Medical Devices Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Device Type

- Market Share, By End Use

- Competitive Outlook and Company Profiles

- Grifols

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Werfen

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Palex Medical

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Siemens Healthineers

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Roche Diagnostics

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- GE HealthCare

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Philips Healthcare

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Medtronic Ibérica

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- B. Braun Medical

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Smith & Nephew

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Stryker Iberia

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Arthrex España

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Hologic España

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Baxter Spain

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Edwards Lifesciences

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Canon Medical Systems

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Others

- Grifols

- Contact Us and Disclaimer

Top Key Players & Market Share Outlook

- Grifols

- Werfen

- Palex Medical

- Siemens Healthineers

- Roche Diagnostics

- GE HealthCare

- Philips Healthcare

- Medtronic Ibérica

- B. Braun Medical

- Smith & Nephew

- Stryker Iberia

- Arthrex España

- Hologic España

- Baxter Spain

- Edwards Lifesciences

- Canon Medical Systems

Frequently Asked Questions