Build Your Custom Market Intelligence Report

Customize Your ReportChina Needle Coke Market Key Highlights

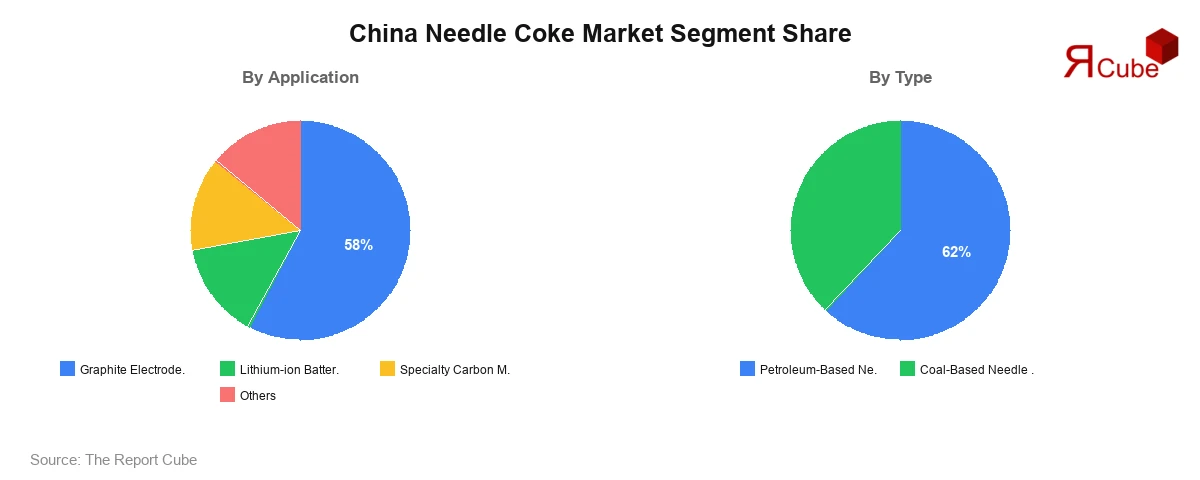

By Type:

Petroleum-Based Needle Coke segment lead the market, with around 62% share.

By Application:

Graphite Electrodes segment dominate the market, accounting for nearly 58% of total revenue.

Regional Outlook:

East China region dominates the market, with around 36% share.

Government Initiatives & Policies

- Made in China 2025 Initiative: Focuses on advanced materials including carbon-based products.

- Dual Carbon Policy (Carbon Peak & Neutrality Goals): Encourages energy-efficient materials and EV battery supply chains.

China Needle Coke Market Insights & Analysis

The China Needle Coke Market is anticipated to register a 10.1% during 2026-2034. the market size was valued at USD 1.45 Billion and is projected to reach USD 3.45 Billion by 2034.

The market is witnessing strong momentum driven by expanding steel production and the accelerating electric vehicle ecosystem across China. Needle coke, a critical raw material for graphite electrodes and lithium-ion battery anodes, has become strategically important as China continues to dominate global steel output, contributing over 50% of global production. The increasing adoption of electric arc furnaces (EAFs), which consume nearly 2.5–3.0 kg of graphite electrodes per ton of steel, is significantly boosting demand for high-quality needle coke.

Additionally, the rapid expansion of China’s EV market, which recorded over 9 million EV sales in 2025, is creating sustained demand for battery-grade needle coke used in anode materials. Government-backed investments in battery manufacturing hubs across provinces like Jiangsu and Guangdong are further strengthening supply chain integration. Domestic producers are scaling production capacities, with new facilities adding over 400 kilotons annually between 2024 and 2026.

China Needle Coke Market Dynamics

Key Driver:

- Rising electric arc furnace steel production increasing graphite electrode demand

- Rapid growth in lithium-ion battery manufacturing for EVs

- Government support for advanced carbon material production

Industry Trends:

- Shift toward premium and super-premium needle coke grades

- Integration of refining and battery material supply chains

- Adoption of cleaner, low-emission production technologies

Book your FREE 30-minute expert consultation today

Contact UsMajor Challenge:

- Volatility in crude oil and coal tar feedstock prices

- Environmental compliance costs impacting smaller producers

- Limited availability of high-quality raw materials

Opportunity:

- Expansion of EV battery manufacturing capacity

- Export potential for high-grade needle coke

- Technological innovation in synthetic graphite production

China Needle Coke Market Segment-wise Analysis

By Type:

- Petroleum-Based Needle Coke

- Coal-Based Needle Coke

Out of all segments, petroleum-based needle coke dominates the market, accounting for nearly 62% share. This dominance is attributed to its superior physical properties, including lower thermal expansion and higher graphitization performance, making it ideal for graphite electrode production. In 2025, petroleum-based variants contributed over USD 0.9 billion in revenue, supported by strong demand from steel manufacturers utilizing EAF technology. Additionally, refiners are increasingly optimizing feedstock blends to enhance yield efficiency by nearly 12–15%, improving cost competitiveness. The segment also benefits from growing adoption in battery-grade applications, where consistency and purity are critical, further reinforcing its leadership position.

By Application:

- Graphite Electrodes

- Lithium-ion Battery Anodes

- Specialty Carbon Materials

- Others

Graphite electrodes represent the leading application segment, holding approximately 58% market share. The segment’s growth is closely tied to China’s steel industry, which produced over 1 billion tons of crude steel in recent years. Graphite electrodes require high-grade needle coke for optimal conductivity and durability, resulting in consistent consumption. The segment has also benefited from increased replacement cycles, as electrodes typically last 8–10 hours in EAF operations. Furthermore, improvements in electrode efficiency have reduced energy consumption by nearly 5%, encouraging wider adoption. The segment continues to expand alongside infrastructure development and industrial output growth across China.

Regional Projection of China Needle Coke Industry

- North China

- East China

- South China

- West China

Among all regions, East China dominates the market, accounting for approximately 36% of the total share. The region benefits from a highly developed industrial base, particularly in provinces such as Jiangsu, Zhejiang, and Shanghai, where battery manufacturing and advanced material industries are concentrated. East China contributes nearly 40% of the country’s lithium-ion battery output, driving substantial demand for high-grade needle coke. Additionally, the presence of large-scale refineries and integrated supply chains improves production efficiency by nearly 10–12%, reinforcing its leading position in the market.

China Needle Coke Market Recent Developments

- 2025: Sinosteel Corporation expanded its high-performance needle coke production capacity by 120 kilotons annually, focusing on supplying premium-grade materials for lithium-ion battery manufacturers and enhancing export capabilities to Southeast Asia.

- 2025: Fangda Carbon New Material Co., Ltd. launched a new ultra-low sulfur needle coke product line, targeting high-end graphite electrode applications and improving thermal stability performance by nearly 18%.

- 2025: CNPC Jinzhou Petrochemical Company upgraded its refining technology with advanced delayed coking units, increasing production efficiency and reducing emissions by approximately 10%, aligning with national sustainability targets.

- 2025: Baosteel Chemical Co., Ltd. entered a strategic partnership with battery manufacturers to supply customized needle coke grades, strengthening vertical integration within China’s EV supply chain ecosystem.

- 2025: Shandong Yida New Material Co., Ltd. invested in R&D facilities to develop next-generation needle coke suitable for high-density battery anodes, improving energy density performance by around 12%.

Build Your Custom Market Intelligence Report

Customized Your ReportWhy Choose This Report?

- Provides a comprehensive overview of the overall market analysis, encompassing key trends, consumer behavior analysis, and risk assessment to support strategic decision-making.

- Provides accurate, up-to-date insights into market size, segmentation, and emerging opportunities, helping to minimize risk & capitalizing on growth.

- Gives deep understanding of target audience preferences, investment habits, and communication channels for enhanced product development & marketing effectiveness.

- Delivers competitive analysis & benchmarking, uncovering the strengths & weaknesses of market competitors to guide strategies.

- Consolidate comprehensive market intelligence, reducing reasoning & streamlining research efforts.

- Facilitates customized market segmentation & risk mitigation strategies, fine-tuned to the business objectives.

- Aids in identifying both market challenges & untapped opportunities within the industry to drive long-term business growth.

- Provides valuable information based on actual customer data & search trends.

Table of Contents

- Introduction

- Objective of the Study

- Product and Category Definition

- Market Segmentation

- Study Variables

- Research Methodology

- Secondary Data Points

- Breakdown of Secondary Sources

- Primary Data Points

- Breakdown of Primary Interviews

- Secondary Data Points

- Executive Summary

- Market Dynamics

- Drivers

- Challenges

- Opportunity Assessment

- Recent Trends and Developments

- Regulatory and Policy Landscape

- China Needle Coke Market Overview (2026-2034)

- Market Size, By Value (USD Billion)

- Market Share, By Type

- Petroleum-Based Needle Coke

- Coal-Based Needle Coke

- Market Share, By Grade

- Intermediate Premium Grade

- Premium Grade

- Super Premium Grade

- Market Share, By Application

- Graphite Electrodes

- Lithium-ion Battery Anodes

- Specialty Carbon Materials

- Others

- Market Share, By End User

- Steel Industry

- Energy Storage Industry

- Aerospace and Defense

- Electronics

- Others

- Market Share, By Distribution Channel

- Direct Sales

- Distributors

- Online Sales

- Market Share, By Region

- North China

- East China

- South China

- West China

- Market Share, By Company

- Revenue Shares and Analysis

- Competitive Landscape

- North China Needle Coke Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Type

- Market Share, By Application

- Market Share, By Grade

- East China Needle Coke Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Type

- Market Share, By Application

- Market Share, By Grade

- South China Needle Coke Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Type

- Market Share, By Application

- Market Share, By Grade

- West China Needle Coke Market

- Market Size, By Value (USD Billion/Million)

- Market Share, By Type

- Market Share, By Application

- Market Share, By Grade

- Competitive Outlook and Company Profiles

- Sinosteel Corporation

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Shanxi Hongte Coal Chemical Co., Ltd.

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Fangda Carbon New Material Co., Ltd.

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- CNPC Jinzhou Petrochemical Company

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Shandong Yida New Material Co., Ltd.

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Baosteel Chemical Co., Ltd.

- Company Overview

- Product Portfolio

- Strategic Alliances/Partnerships

- Recent Developments

- Sinosteel Corporation

- Contact Us and Disclaimer

List of Figure

List of Table

Top Key Players & Market Share Outlook

- Sinosteel Corporation

- Shanxi Hongte Coal Chemical Co., Ltd.

- Fangda Carbon New Material Co., Ltd.

- CNPC Jinzhou Petrochemical Company

- Shandong Yida New Material Co., Ltd.

- Baosteel Chemical Co., Ltd. &

- Others

Frequently Asked Questions